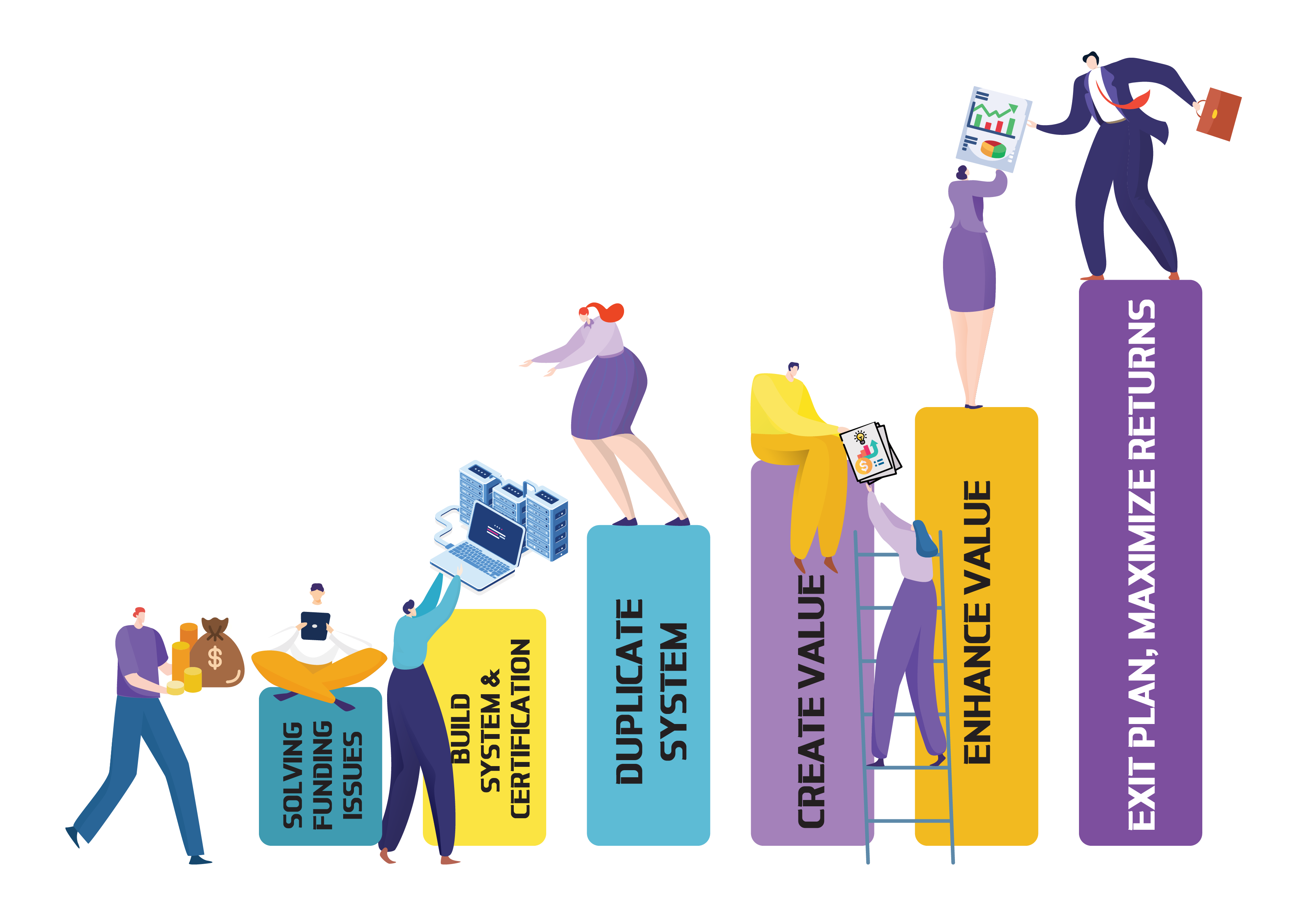

Customize Your Financing Solution Quickly and Efficiently

Reducing The Possibility of Loan Rejection

Expedite The Process of Disbursement

Enhancing Your Possibility of Loan Approval

Responsible and Confident Assurance

100% Approved

>20Years

>12,810 Approval

>7,405 Millions Fund Disbursed

Most Government Endorsements

Platform of Highly Knowledgeable, Exceptionally Informative & Distinctly Connected People

Trained Many Popular Loan Consultants and Credit Officers

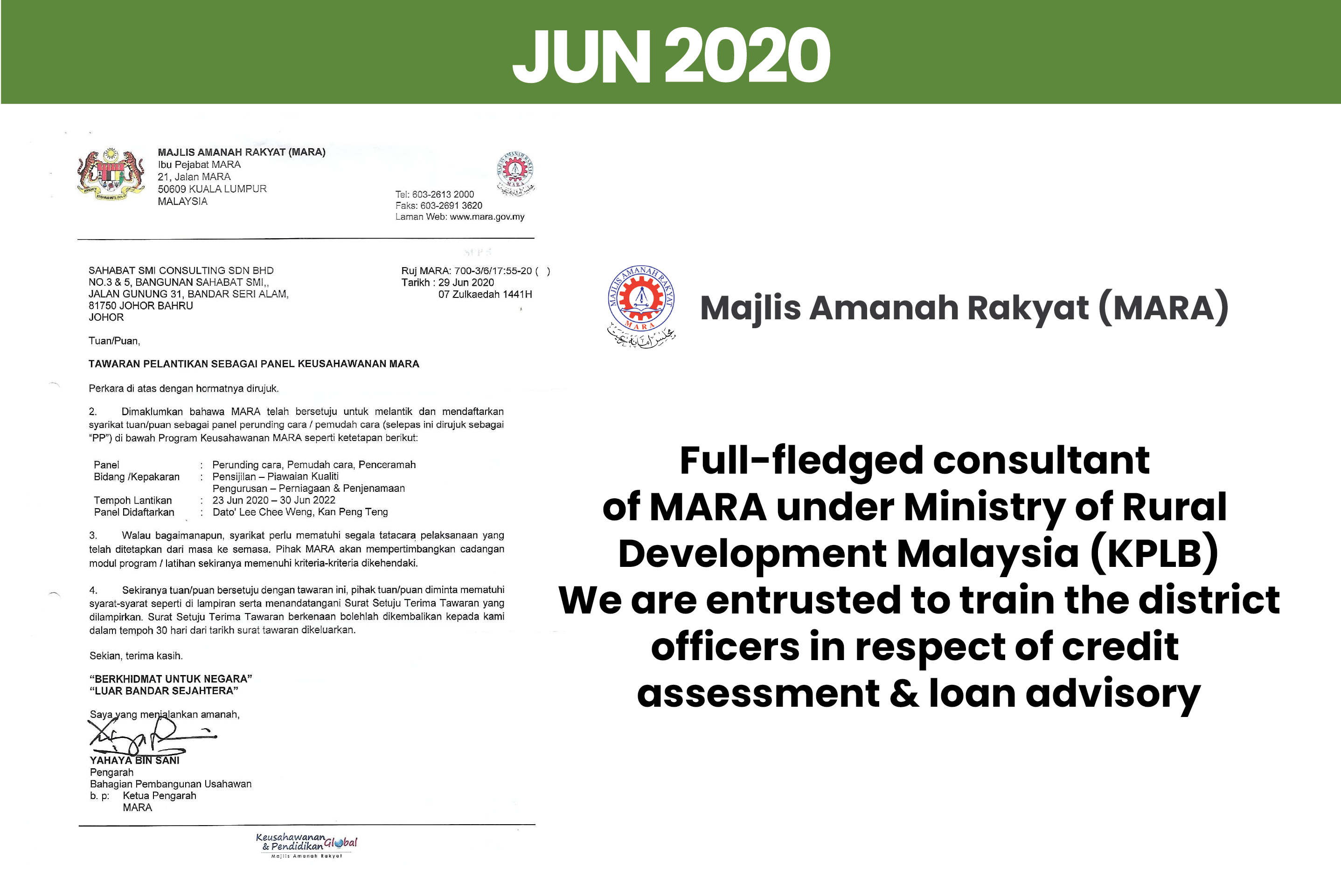

SSMI 1.0 (Phase 01) : Solving All Your Funding Issues

Since 2004, SAHABAT SMI Consulting has consistently set industry standards, achieving numerous records and milestones, inspiring others to strive for excellence. With over 12,000 cases approved and RM7 billion in value, they've embarked on a transformative Phase 2, recognizing that business success involves more than just financing.

SSMI 2.0 (Phase 02) : Establishment of the 5 Essential Elements

Since 2004, SAHABAT SMI Consulting has consistently set industry standards, achieving numerous records and milestones, inspiring others to strive for excellence. With over 12,000 cases approved and RM7 billion in value, they've embarked on a transformative Phase 2, recognizing that business success involves more than just financing.

SSMI 3.0 (Phase 03) : Establishment of Entrepreneurial Incubation Platform

Leveraging years of successful experience and strong government ties, SAHABAT SMI ® has built trust with Entrepreneur Development Agencies. With a robust resource integration platform, they invite trustworthy entrepreneurs to join and contribute to the economy's growth.

Corporate Video